See your cancer insurance coverage options.

Cancer insurance – financial help during your journey to recovery

The costs of living with cancer are hard to predict. A cancer insurance policy can go beyond your health insurance to provide funds that help cover a wide range of expenses – both medical and non-medical – when you need support most.

According to the American Cancer Society, about one out of every two men and one out of every three women will develop cancer at some point. The medical expenses associated with cancer treatment will generally mean that cancer patients end up having to meet a comprehensive health plan’s deductible and out-of-pocket cap, which can be as high as $9,450 for a single person’s in-network care in 2024.1

If you undergo treatment for cancer, you may find that you need to take extended time away from work, and possibly travel to a different area to receive the care you need. That can create a significant financial burden – even if you have robust medical coverage.

The financial impact of cancer adds additional stress to an already stressful situation, and a study by Dr. Veena Shankaran, a University of Washington oncologist, and other researchers found cancer patients are 2.5 times more likely to declare bankruptcy than people who haven’t had cancer.

What is cancer insurance?

Cancer insurance, also known as specified-disease insurance in some states, is a type of supplemental health insurance that pays cash benefits for various cancer diagnoses and treatments. You can use that money to pay out-of-pocket medical costs and other expenses, including travel, lodging and meals during treatment, child care and home health services.

Cancer insurance is intended to supplement a comprehensive major medical health plan, and is not suitable to be a person’s only coverage for healthcare.

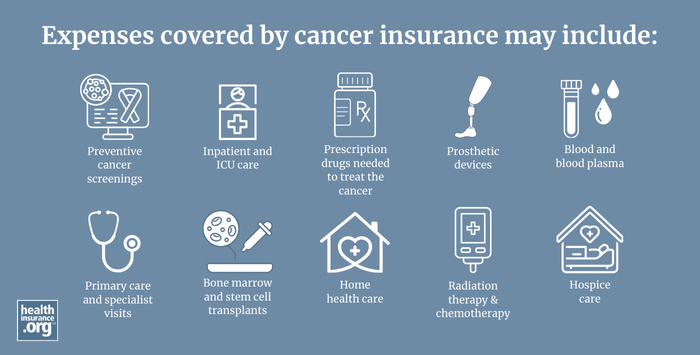

Expenses covered by cancer insurance may include:

Preventive cancer screenings

Inpatient and ICU care

Surgery, including reconstructive surgery, and any necessary anesthesia

Prescription drugs needed to treat the cancer or side effects of the treatment

Radiation therapy, chemotherapy, and immunotherapy

Bone marrow and stem cell transplants

Primary care and specialist visits

Transportation by ambulance

Blood and blood plasma

Prosthetic devices

Skilled nursing and rehabilitation care

Home health care

Hospice care

{kind=link}

Frequently asked questions about cancer insurance

How does cancer insurance work?

Unlike major medical policies, which send payments directly to medical providers, cancer insurance policies send benefits to the policyholder (or policyholder’s assignee) to use as they see fit. Cancer insurance plans can pay benefits as a single lump sum, or as a set amount for various specific treatments under a scheduled benefits policy.

- A lump sum policy pays a predetermined amount of money if you’re diagnosed with cancer, regardless of the subsequent treatments that you may need. This can often be added as a rider to a scheduled benefits policy.

- A scheduled benefits policy (also called an indemnity policy) has separate predetermined benefit amounts that you can receive when you have various specific cancer treatments, such as inpatient care, surgery, anesthesia, bone marrow or stem cell transplants, chemotherapy and radiation. (Some plans pay a percentage of incurred costs for specific treatments up to a specified cap, but these are not as common.)

Insurers can offer different levels of coverage, with more expensive policies paying higher benefit amounts. But all cancer insurance policies pay out specified amounts, regardless of your actual costs. This is is why it’s so important to also maintain comprehensive major medical coverage, which does not have a cap on how much it will pay for medically necessary care.

What does cancer insurance cover?

The specifics vary from one plan to another, and each state regulates the benefits allowed by these plans. If a policy pays benefits for specific treatments, it’s common to see payouts for a wide range of medical services, including:

- Preventive cancer screenings

- Inpatient and ICU care

- Surgery, including reconstructive surgery, and any necessary anesthesia

- Prescription drugs needed to treat the cancer or side effects of the treatment

- Radiation therapy, chemotherapy, and immunotherapy

- Bone marrow and stem cell transplants

- Primary care and specialist visits

- Transportation by ambulance

- Blood and blood plasma

- Prosthetic devices

- Skilled nursing and rehabilitation care

- Home health care

- Hospice care

What doesn't cancer insurance cover?

What factors should I consider when choosing cancer insurance?

Who’s selling the policy?

Make sure the cancer policy insurer (and agent, if you’re using one) is licensed in your state.

Type of payment

Will the policy pay a lump sum if you’re diagnosed with cancer, or smaller amounts for a variety of different treatments?

Conditions covered

Will the plan pay anything if you need treatment for a separate condition that’s related to the cancer or cancer treatment?

Coverage of non-medical expenses

Will it provide a benefit for non-medical expenses, such as child care, pet care/boarding, or travel/lodging?

What companies offer cancer insurance?

There are numerous insurance companies that offer cancer insurance for individuals and families. In some cases, consumers can purchase cancer policies directly from an insurer’s website, while enrollment in other plans – such as employer-sponsored plans – may require the buyer to work with a health insurance agency or brokerage.

Can I get cancer insurance if I already have cancer?

In general, no, unless you’re enrolling in a group cancer/critical illness supplement offered by an employer. (Those plans are generally guaranteed-issue, regardless of medical history.) If you’re buying your own coverage, cancer insurance is something you’d need to purchase before you get cancer.

Thanks to the Affordable Care Act, individual major medical health insurance is guaranteed-issue and covers pre-existing conditions. But supplemental insurance, including cancer policies, is among the excepted benefits excluded by the ACA, and does not have to cover pre-existing conditions. These plans can have waiting periods before benefits can be payable, and they can also deny an application due to medical history.

Depending on the insurer’s underwriting rules, a person who had cancer may have to have been been cancer-free for several years may be able to purchase a cancer insurance policy. It’s important to review the terms of your cancer insurance policy.

Will a cancer insurance policy cover my current doctors?

There are no provider networks for cancer insurance policies, since plans pay benefits directly to the policyholder, who can use the funds for whatever purpose they choose. But to minimize your out-of-pocket costs, it’s in your best interest to use medical providers who are in-network with your major medical health plan.

Is cancer insurance worth it?

This depends on your circumstances. There are several things to consider when you’re deciding whether you should buy a cancer insurance policy:

- How much is your health plan’s out-of-pocket limit, and would having to pay it be a financial hardship?

- Are there more robust health plans available to you, and if so, would it make more sense to spend more on your major medical coverage, instead of supplementing with a cancer insurance policy?

- Do you have a well-funded health savings account (HSA) or emergency fund?

- Do you have a generous paid sick leave policy from your employer, or disability insurance that will cover a portion of your income if you have to take time off work due to cancer treatment?

- If you’re also considering life insurance, do the insurers offer the option to add a cancer rider or critical illness rider to the plan? If so, that can be an economical way to combine life insurance and supplemental health benefits.

- Do you live near good cancer treatment facilities, or is it likely that you might need to travel for treatment?

- Do you have a family history of cancer?

- You know your own circumstances better than anyone. If the financial impact of cancer would likely be stressful, a supplemental cancer insurance policy might add to your peace of mind.

How does cancer insurance differ from critical illness insurance?

Cancer insurance policies will only pay benefits if the policyholder is diagnosed with a covered type of cancer. Critical illness policies (sometimes called “dread disease” policies) are based on a similar concept, but provide benefits for a broader scope of diseases.

Critical illness policies all have specific lists of illnesses that will trigger a payout. Most types of cancer are generally included, along with conditions like heart attack, stroke, or organ failure/transplant.

If the benefit payout amounts are roughly equal, a critical illness policy will generally cost more than a cancer policy, simply because it provides benefits for more medical conditions and thus is more likely to result in a benefit being paid to the policyholder.

If you’re shopping for a cancer insurance policy, you may see the option to add a critical illness rider to the policy. This would increase the premium, but would also expand the scope of medical conditions for which you could receive cash benefits.

Are cancer insurance benefits taxable?

You should contact a financial or accounting professional for guidance about your specific situation. In general, however, the answer depends on whether you got the policy through your employer or purchased it on your own. If you purchase your own cancer insurance policy and pay the premiums with after-tax dollars, benefits you receive under the policy are not taxable. If you’re enrolled in an employer’s group cancer policy and the premiums are paid pre-tax, the benefits can be taxed and you may receive documentation indicating the amount of the taxable benefit that you received.

In 2017, the IRS clarified that if you receive benefits under an employer’s fully insured fixed indemnity benefit plan, you only have to pay taxes on the amount that exceeds your out-of-pocket medical expenses. So, for example, if your health plan has a $25 copay for an office visit and your group cancer policy (paid with pre-tax dollars) pays a $100 benefit for an office visit related to cancer treatment, only $75 of that benefit would be taxable.

The IRS proposed new rules in 2023 that would have made benefits received under a fixed indemnity or specified disease policy (without regard for the actual amount of medical expenses incurred) taxable if the premiums were paid pre-tax, as is often the case for employer-sponsored supplemental insurance. This would have made the benefits subject to FICA, FUTA, and income tax withholding. But that proposed rule was not finalized.5

Looking for more information about supplemental options?

Is supplemental coverage right for you?

Supplemental coverage – such as accident insurance, critical illness insurance, vision insurance and travel insurance – can pick up where major medical leaves off.

Speak to a licensed insurance agent at one of our agency partners.

Footnotes

- ”Premium Adjustment Percentage, Maximum Annual Limitation on Cost Sharing, Reduced Maximum Annual Limitation on Cost Sharing, and Required Contribution Percentage for the 2024 Benefit Year” Centers for Medicare & Medicaid Services. Dec. 12, 2022. ⤶

- Cancer Facts & Figures 2024. American Cancer Society. Accessed February, 2024. ⤶

- A Shopper's Guide to Cancer Insurance. NAIC. Accessed February, 2024. ⤶

- Financial Toxicity (Financial Distress) and Cancer Treatment. National Cancer Institute. Accessed February, 2024. ⤶

- Short-Term, Limited-Duration Insurance and Independent, Noncoordinated Excepted Benefits Coverage Internal Revenue Service; Employee Benefits Security Administration; Health and Human Services Department. April 3, 2024 ⤶