What is coordination of benefits?

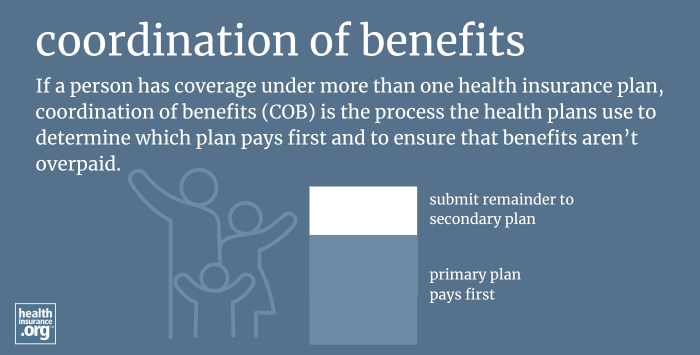

If a person has coverage under more than one health insurance plan, coordination of benefits (COB) is the process the health plans use to determine which plan pays first and to ensure that benefits aren’t overpaid.1

If you have coverage under two or more health plans, one will be the “primary payer” and the others will be the “secondary payers.”

- If you have a claim for which you are entitled to receive benefits under multiple plans, the primary payer will provide coverage according to its schedule of benefits.

- A secondary payer will then process the claim after accounting for payments made by the primary payer. The secondary payer plan can help to cover out-of-pocket costs left over after the primary plan processes the claim. But coordination of benefits ensures that the secondary plan isn’t duplicating payments made by the primary plan.

- Both plans will provide an explanation of benefits (EOB), clarifying how the claim was processed and what the plan paid.

If you only have health coverage under one plan, the coordination of benefits provisions of your coverage will not apply. However, your health plan may periodically ask you for updated information to confirm whether you have any additional coverage.

How can I tell which plan is primary and which is secondary?

Determining which plan is primary and which is secondary will depend on the type of coverage you have.

Medicaid

Medicaid is always a secondary payer plan.2 So, if a person has Medicaid in addition to other coverage, the other coverage will always be the primary payer.

Medicare

If a person has Medicare and an employer group health plan, Medicare is the primary payer if the employer has fewer than 20 employees, but secondary if the employer has 20 or more employees. (There are different rules if the person is eligible for Medicare due to a disability, ALS, or ESRD).3

Private health insurance

If a person has coverage under more than one private health plan, COB protocols will typically be outlined in each plan’s summary of benefits and coverage.

To provide clarification and standardization, many states have either implemented state-specific COB rules, or adopted the National Association of Insurance Commissioners’ (NAIC) Coordination of Benefits Model Regulation.4 This model regulation addresses numerous COB situations.5 Some of the most common rules are:

- If a person is covered under one plan as an employee and another as a spouse or dependent, the plan that covers them as an employee will be primary and the other will be secondary.

- If a person is covered under one plan as an active employee and another plan as a retired or laid-off employee, or through COBRA (or other continuation) coverage, the active employee coverage will be primary.

- If a child is covered by both parents’ employer-sponsored plans, the “birthday rule” calls for primary coverage to be provided by the plan of the parent whose birthday comes first in each calendar year.

- If there are no specific rules that apply to a particular situation, the plan that has provided coverage to the person for a longer period of time will be primary.

Do all types of health coverage use coordination of benefits?

No. Some types of supplementary coverage do not utilize coordination of benefits. For example, critical illness insurance and fixed-indemnity plans, each a type of coverage that pays a cash benefit when an insured receives a qualifying diagnosis or medical service, are exempt from various health insurance rules only as long as they do not utilize coordination of benefits.6

Say you have a critical illness policy that will pay a $10,000 cash benefit if you’re diagnosed with an internal cancer. If you are diagnosed with a cancer that’s covered by the critical illness plan, you’ll receive a $10,000 payout from that plan, regardless of whether you have major medical health insurance, the terms of that coverage, or your actual costs. These fixed-benefit plans make it clear that you can use the cash benefit for anything you like.

In contrast, if you had two major medical plans that utilized coordination of benefits, the secondary payer would not have paid more than your out-of-pocket costs after the primary payer had processed the claim.

Footnotes

- “Coordination of Benefits Model Regulation” National Association of Insurance Commissioners. Accessed Feb. 26, 2025 ⤶

- “Coordination of Benefits & Third Party Liability” Medicaid.gov. Accessed Feb. 26, 2025 ⤶

- “Medicare Secondary Payer” Medicare.gov. Accessed Feb. 26, 2025 ⤶

- “Coordination of Benefits Model Regulation – State Pages” National Association of Insurance Commissioners. Accessed Feb. 26, 2025 ⤶

- “Coordination of Benefits Model Regulation” National Association of Insurance Commissioners. Accessed Feb. 26, 2025 ⤶

- “Short-Term, Limited-Duration Insurance and Independent, Noncoordinated Excepted Benefits Coverage” Internal Revenue Service; Employee Benefits Security Administration; Health and Human Services Department. Federal Register. April 3, 2024 ⤶