Inflation Reduction Act

What is the Inflation Reduction Act?

The Inflation Reduction Act (IRA) was signed into law by President Biden in August 2022. Although the IRA’s most significant investments were related to climate change, the law also made numerous important improvements to health coverage.

How does the Inflation Reduction Act help people who buy their own health coverage?

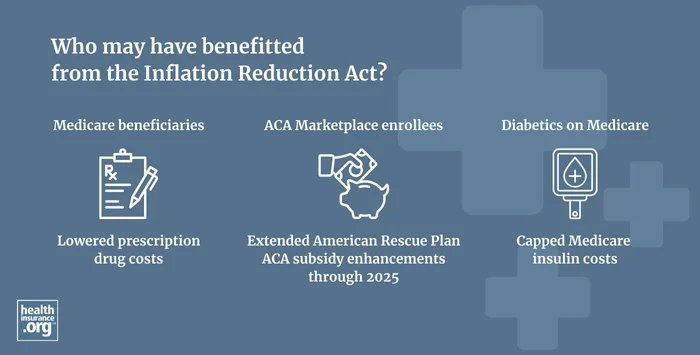

Under the IRA, the American Rescue Plan's (ARP) enhancements of the ACA's premium tax credits (subsidies) were extended through the end of 2025. Without the IRA, they would have expired at the end of 2022.

Congress failed to further extend the ARP subsidy enhancements in December 2025, so they expired at the end of 2025. This issue could be revisited at some point in 2026. But for the time being, premium tax credits continue to be available in the Marketplace in 2026, but they follow the ACA's rules rather than the enhanced subsidy rules that the ARP temporarily put in place.

- Because of the IRA, the “subsidy cliff” continued not to be a problem through the end of 2025, meaning subsidies were available even if household income was more than 400% of the federal poverty level. And subsidies continued to be larger than they would otherwise have been. Both of these provisions expired at the end of 2025, as Congress did not extend them again.

- The IRA also allowed the year-round enrollment opportunity for subsidy-eligible low-income households to continue to be available, although access to this special enrollment ended in 2025 under new federal rules.

- Some of the American Rescue Plan’s subsidy provisions had already expired by the end of 2021. They included a COBRA subsidy, unemployment-related subsidies, and a one-time amnesty from having to repay excess premium subsidies to the IRS. None of these provisions were revived by the IRA.

Nearly 23.4 million people were enrolled in health coverage through the Marketplace (exchange) as of early 2025.1 Nearly all of them – 93% – were receiving advance premium tax credits. These tax credits were larger and more widely available than they would have been without the Inflation Reduction Act. But as noted above, the subsidy enhancements expired at the end of 2025, and are not available for 2026. (This issue is still under consideration by Congress in early 2026, so this could still change.)

Read our overview of the IRA provisions that affected ACA Marketplace health plan buyers.

How does the Inflation Reduction Act help Americans with Medicare coverage?

The IRA includes numerous provisions that have improved Medicare’s prescription drug coverage, with changes that began phasing in starting in 2023. Unlike the Marketplace changes described above, the Medicare changes are permanent and do not need to be reauthorized.

These changes affect more than 56 million2 people enrolled in Medicare Part D coverage, either as a stand-alone plan or as part of a Medicare Advantage plan – and have also improved pharmaceutical benefits some Medicare enrollees receive under Medicare Part B.

IRA provisions affecting Medicare drug coverage include:

- Recommended vaccines covered by Medicare Part D no longer have any out-of-pocket costs.

- Copays for all covered insulin products are capped at $35/month (including Part B coverage of insulin for use in insulin pumps)

- For drugs covered under Part B (infusion or injection drugs given in a clinic or medical office), drug manufacturers have to pay rebates to Medicare if drug prices increase faster than inflation, and enrollees pay lower coinsurance (normally 20%) for those drugs.

- Out-of-pocket costs in the Medicare Part D catastrophic coverage phase were eliminated starting in 2024.

- Out-of-pocket costs under Medicare Part D are capped at $2,000 starting in 2025 (adjusted for inflation in future years; the cap is $2,100 in 2026).3

- The full Part D Low-Income Subsidy (Extra Help) became available to more enrollees.

- CMS negotiations with drug manufacturers over the price of certain high-cost prescription drugs. The first round of negotiated prices takes effect in 2026, for ten high-cost drugs.4

Read a full overview of the IRA provisions that affect Medicare enrollees.

Footnotes

- "Effectuated Enrollment: Early 2025 Snapshot and Full Year 2024 Average" CMS.gov, July 24, 2025 ⤶

- "Medicare Monthly Enrollment, September 2025" Centers for Medicare & Medicaid Services. Accessed Dec. 29, 2025 ⤶

- "How much does Medicare drug coverage cost?" Medicare.gov. Accessed Dec. 29, 2025 ⤶

- "Selected Drugs and Negotiated Prices" Centers for Medicare & Medicaid Services. Accessed Dec. 29, 2025 ⤶