Medicare in Ohio

Ohio has no provisions to ensure access to Medigap plans for disabled Medicare beneficiaries under age 65

Key takeaways

- Over 2.5 million residents are enrolled in Medicare in Ohio.1

- 56% of Ohio Medicare beneficiaries are enrolled in Medicare Advantage plans.1

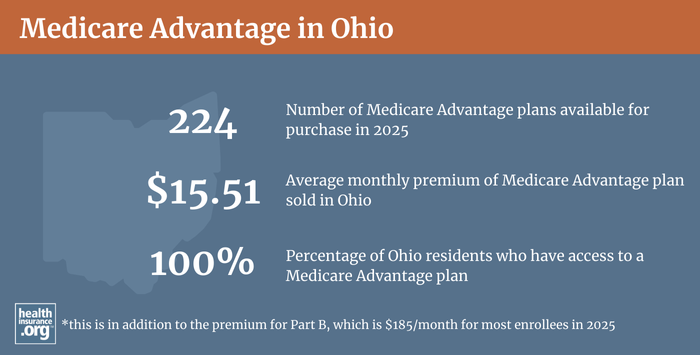

- Ohio has a more robust Medicare Advantage market than many other states, with plans available in every county.2

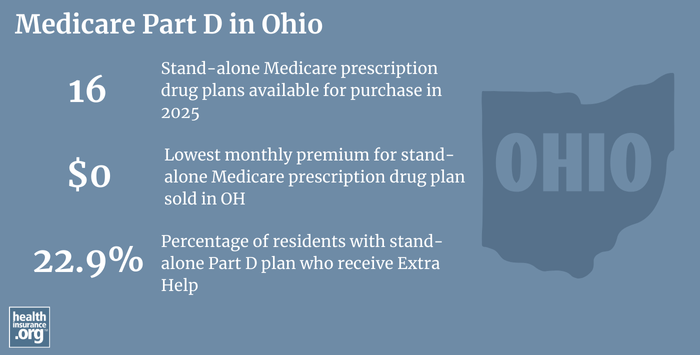

- There are 16 stand-alone Part D prescription plans available in Ohio in 2025, with premiums starting at $0 per month.3

Ohio Medicare enrollment

As of September 2024, there were 2,534,552 residents covered by Medicare in Ohio,1 amounting to nearly 19% of the state’s population.4

For most individuals, Medicare coverage enrollment goes along with turning 65. But Medicare eligibility is also triggered for younger people if they have been receiving disability benefits for 24 months, or have end stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS). Nationwide, about 11% of Medicare beneficiaries — over 7 million people — are under age 65.5 In Ohio, about 12% of Medicare beneficiaries are under 65.1

Learn about Medicare plan options in Ohio by contacting a licensed agent.

Explore our other comprehensive guides to coverage in Ohio

We’ve created this guide to help you understand the Ohio health insurance options available to you and your family, and to help you select the coverage that will best fit your needs and budget.

Hoping to improve your smile? Dental insurance may be a smart addition to your health coverage. Our guide explores dental coverage options in Ohio.

Learn about Ohio’s Medicaid expansion, the state’s Medicaid enrollment and Medicaid eligibility.

Short-term health plans provide temporary health insurance for consumers who may find themselves without comprehensive coverage. Learn more about short-term plan availability in Ohio.

Frequently asked questions about Medicare in Ohio

What is Medicare Advantage?

Medicare beneficiaries can choose to get their healthcare coverage through Medicare Advantage plans, or directly from the federal government via Original Medicare. There are pros and cons to either option, and the right solution is different for each person.

Medicare Advantage plans are offered by private insurers, so plan availability varies from one area to another. There are Medicare Advantage plans in all counties in Ohio,2 and the state’s Medicare Advantage market offers more than many other states.2 For 2025, all Ohio Medicare beneficiaries can select from among at least 36 Medicare Advantage plans, residents in most Ohio counties have access to 50+ Medicare Advantage plans.2

As of September 2024, more than 56% of all Ohio Medicare beneficiaries had Medicare Advantage. plans1 The other almost 46% of Ohio Medicare beneficiaries were enrolled in Original Medicare.1

The Medicare Annual Election Period (October 15 to December 7 each year) allows Medicare beneficiaries the chance to switch between Medicare Advantage and Original Medicare (and add, drop, or switch to a different Medicare Part D prescription drug plan). People who are already enrolled in Medicare Advantage also have the option to switch to a different Medicare Advantage plan or to Original Medicare during the Medicare Advantage Open Enrollment Period, which runs from January 1 to March 31.

What is Medigap?

Original Medicare does not limit out-of-pocket costs, so most enrollees maintain some form of supplemental healthcare coverage. Nationwide, more than 80% of Original Medicare beneficiaries have a supplemental plan.6 But for those who don’t, optional Medigap plans (also known as Medicare supplement insurance plans, or MedSupp) will pay some or all of the out-of-pocket costs they would otherwise have to pay if they had Original Medicare on its own and experienced a medical claim.

According to America’s Health Insurance Plans (AHIP) analysis, there were 609,691 Ohio Medicare beneficiaries who had Medigap coverage as of 2022.7 In many states, there has been a steady downward trend in Medigap enrollment in recent years as Medicare Advantage plans have gained popularity (Medigap plans cannot be used with Medicare Advantage plans, so fewer people have Medigap plans when Medicare Advantage plan enrollment increases).

Medigap plans are sold by private insurers, but they’re standardized under federal rules (so each plan will provide the same benefits as any other plan labeled with the same letter; Plan G, Plan K, etc.) and regulated by state laws and insurance commissioners. In Ohio, there are 48 insurers offering Medigap plans.8 The Medicare website has a plan finder tool that will show you prices and plan availability for the various Medigap plans that can be purchased in Ohio.

Federal rules require Medigap insurers to offer plans on a guaranteed-issue basis during an enrollee’s Open Enrollment Period, which begins when the person is at least 65 years old and enrolled in Medicare Part A and Medicare Part B. But despite the fact that nearly 8 million Medicare beneficiaries are not yet 65 (and are enrolled in Medicare due to a disability) there is no federal requirement that Medigap insurers offer plans to people who are under age 65.

The majority of the states have addressed this with legislation that ensures at least some access to Medigap plans for people under age 65, but Ohio is not among them. Ohio’s Medicare guide notes that Medigap plans are available on a guaranteed-issue basis for six months after they’re at least 65 and enrolled in Medicare Part A and Part B,9 or when they have a federally-mandated guaranteed-issue right.

As of 2017, the Ohio Department of Insurance published a comprehensive Medigap shopping guide. And although they noted that some insurers in the state did offer Medigap plans to people under 65 (at a higher premium), no insurers submitted under-65 rates to the state for inclusion in the shopping guide. And as of 2023, Medicare’s Medigap plan finder tool indicates that there are no Medigap plans available for Medicare beneficiaries under the age of 65 in Ohio. More than 320,000 Ohio Medicare beneficiaries are under age 65 as of 2023. For this population, the state recommended that they contact Medigap insurers directly (using the phone numbers in the Ohio Medicare premium comparison chart) to see if the insurer will offer them a plan. But it appears that most of them likely will not.

Disabled Medicare beneficiaries have a Medigap open enrollment period when they turn 65. At that point, they can select from among any of the available Medigap plans in their state.

There are several states (including South Carolina, Alaska, Wyoming, Iowa, and Nebraska) that still have operational pre-Affordable Care Act (ACA) high-risk pools that offer coverage to Medicare beneficiaries who are unable to qualify for Medigap plans. The majority of the remaining states require private Medigap insurers to offer at least some plans to disabled enrollees under age 65. But Ohio is among the states that have made no provisions at all to ensure access to supplemental coverage for disabled Medicare beneficiaries. (Note that under federal rules, these beneficiaries do get an open enrollment period for Medigap plans when they turn 65, even if they’ve already been enrolled in Medicare for years due to a disability.)

Under federal rules, disabled Medicare beneficiaries, including those with kidney failure, do have the option to enroll in a Medicare Advantage plan instead of Original Medicare. Medicare Advantage plan monthly premiums are not higher for those under 65. But Medicare Advantage plans may have more limited provider networks than Original Medicare, and total out-of-pocket costs can be as high as $9,350 per year for in-network care, plus the out-of-pocket cost of prescription drugs.10

Although the Affordable Care Act eliminated pre-existing condition exclusions in most of the private health insurance market, those rules don’t apply to Medigap plans. Medigap insurers can impose a pre-existing condition waiting period of up to six months if you didn’t have at least six months of continuous coverage prior to your enrollment (although many of them choose not to do so). And if you apply for a Medigap plan after your initial enrollment window closes (assuming you aren’t eligible for one of the limited guaranteed-issue rights), the Medigap insurer can consider your medical history in determining whether to accept your application, and at what premium.

What is Medicare Part D?

Original Medicare does not provide coverage for outpatient prescription drugs. More than 80% of Original Medicare beneficiaries have a supplemental plan,6 and these plans often include prescription coverage.

But Medicare Part D, created under the Medicare Modernization Act of 2003, provides prescription drug coverage for Medicare beneficiaries who do not have another source of coverage for prescription costs. Medicare Part D coverage can be purchased as a stand-alone Medicare Part D prescription plan or obtained as part of a Medicare Advantage plan with integrated Medicare Part D benefits. Both options are available for purchase (or plan changes) during the Medicare Annual Election Period that runs from October 15 to December 7 each year, with the new coverage effective January 1 of the coming year.

There are 16 stand-alone Medicare Part D plans in Ohio for 2025, with premiums that start at $0/month.3

As of September 2024, 1.2 million had Part D coverage integrated with a Medicare Advantage plan, and just over 900,000 had stand-alone Part D coverage.1

Medicare Part D prescription drug plan enrollment follows the same schedule as Medicare Advantage plan enrollment: People can sign up when they’re first eligible for Medicare, or they can enroll during the Medicare Annual Enrollment Period each fall, which runs from October 15 to December 7. Medicare Part D prescription drug plan enrollment and plan changes made during the fall enrollment period take effect the following January.

How does Medicaid provide financial assistance to Medicare beneficiaries in Ohio?

Many Medicare beneficiaries receive financial assistance through Medicaid with the cost of Medicare premiums and services Medicare doesn’t cover – such as long-term care.

Our guide to financial assistance for Medicare enrollees in Ohio includes overviews of these benefits, including Medicare Savings Programs, long-term care coverage, and eligibility guidelines for assistance.

What additional resources are available for Medicare beneficiaries and their caregivers in Ohio?

Need help with filing for Medicare benefits? Got questions about Medicare eligibility in Ohio? You can contact the Ohio Senior Health Insurance Information Program with questions related to Medicare coverage and enrollment in Ohio.

The Ohio Department of Insurance also has a useful resource page all about Medicare in Ohio. The Department of Insurance oversees, licenses, and regulates health insurance companies and the brokers/agents who sell coverage within the state. They can provide assistance to consumers who have questions or complaints about any entity the Department regulates.

The Medicare Rights Center is a nationwide service (call center and website) that can provide assistance, education, and information to Medicare beneficiaries and their caregivers.

Financial help for Ohio Medicare beneficiaries is a helpful overview of how the state Medicaid program can provide financial assistance for Medicare beneficiaries in a variety of circumstances, based on income and resource/asset levels.

Louise Norris is an individual health insurance broker who has been writing about health insurance and health reform since 2006. She has written dozens of opinions and educational pieces about the Affordable Care Act for healthinsurance.org.

Footnotes

- “Medicare Monthly Enrollment – Ohio.” Centers for Medicare & Medicaid Services Data. Accessed January, 2025. ⤶ ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- ”Medicare Advantage 2025 Spotlight: First Look” KFF.org Nov. 15, 2024 ⤶ ⤶ ⤶ ⤶

- ”Fact Sheet: Medicare Open Enrollment for 2025” (107) Centers for Medicare & Medicaid Services. Sep. 27, 2024 ⤶ ⤶

- U.S. Census Bureau Quick Facts: United States & Ohio.” U.S. Census Bureau, July 2024. ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data. Accessed January, 2025. ⤶

- Ochieng, Nancy, and Jeannie Fuglesten Biniek. “Cost-Related Problems Are Less Common among Beneficiaries in Traditional Medicare than in Medicare Advantage, Mainly Due to Supplemental Coverage.” Kaiser Family Foundation, July 7, 2021. ⤶ ⤶

- ”The State of Medicare Supplement Coverage” AHIP. May 2024 ⤶

- “Explore your Medicare coverage options.” Medicare.gov. Accessed October, 2024. ⤶

- “Medicare 101.” Department of Insurance | ohio.gov, February 2023. ⤶

- ”Final Contract Year (CY) 2025 Standards for Part C Benefits, Bid Review and Evaluation” Centers for Medicare & Medicaid Services. May 6, 2024 ⤶